The blockchain industry stands at a critical crossroads, with an unprecedented $6.8 billion investment pouring into technological advancements. Yet, as this revolutionary technology continues to reshape finance, supply chains, and digital identity systems, a pressing question emerges: Can innovation keep pace with escalating blockchain security risks? Recent data reveals that cryptocurrency hacks and exploits resulted in losses exceeding $3.8 billion in 2024 alone, highlighting the urgent need for robust security measures. As enterprises and governments increasingly adopt distributed ledger technology, understanding the delicate balance between advancement and vulnerability has never been more critical for investors, developers, and everyday users navigating this digital frontier.

Current Blockchain Security Landscape

The Evolution of Blockchain Security Risks

The blockchain ecosystem has matured significantly since Bitcoin’s inception in 2009, yet blockchain security risks have evolved in parallel with technological sophistication. Early vulnerabilities centred primarily on cryptographic weaknesses and 51% attacks. Today’s threat landscape encompasses a complex array of attack vectors, including smart contract exploits, bridge vulnerabilities, oracle manipulation, and social engineering schemes targeting decentralised finance (DeFi) protocols.

Modern blockchain vulnerabilities extend beyond technical flaws to encompass governance issues, regulatory gaps, and human error. The decentralised nature of blockchain networks—while offering unprecedented transparency and resilience—also creates unique security challenges that traditional cybersecurity frameworks struggle to address. Cross-chain bridges, which facilitate interoperability between different blockchain networks, have become particularly attractive targets, accounting for over $2 billion in stolen funds during the past two years.

Major Blockchain Security Risks Categories

Smart Contract Vulnerabilities represent one of the most persistent blockchain security risks. These self-executing programs, while eliminating intermediaries, contain code that can harbour critical flaws. Reentrancy attacks, integer overflows, and logic errors have enabled hackers to drain millions from DeFi protocols. The infamous DAO hack of 2016, which resulted in $60 million in losses, demonstrated how a single vulnerability in smart contract code could threaten an entire ecosystem.

Consensus Mechanism Weaknesses pose fundamental risks to blockchain integrity. While Proof-of-Work systems face 51% attacks where malicious actors gain majority control of network hash power, Proof-of-Stake networks confront different challenges, including “nothing at stake” problems and long-range attacks. Smaller blockchain networks with lower hash rates or stake requirements remain particularly vulnerable to these consensus-level exploits.

Private Key Management Issues continue to plague both individual users and institutional investors. Unlike traditional banking systems with recourse mechanisms, blockchain transactions are irreversible. Lost or stolen private keys mean permanent loss of assets. Exchange hacks, phishing attacks, and malware targeting wallet software have resulted in billions in losses, emphasising the critical importance of secure key storage solutions.

Oracle Manipulation threatens blockchain applications requiring real-world data. Decentralised oracles that feed external information to smart contracts can be compromised, leading to incorrect contract executions. Flash loan attacks exploiting oracle price feeds have become increasingly sophisticated, allowing attackers to manipulate market data within single blockchain transactions.

The $6.8 Billion Investment: Catalysing Innovation or Playing Catch-Up?

Where the Money Is Going

The $6.8 billion investment in blockchain advancement flows through multiple channels, each targeting specific aspects of security and functionality. Venture capital firms have allocated substantial funds toward developing next-generation consensus mechanisms that promise enhanced security without sacrificing decentralisation or performance. Projects implementing zero-knowledge proofs, multi-party computation, and advanced cryptographic techniques attract significant investor attention.

Infrastructure development receives considerable funding, particularly for Layer 2 scaling solutions that aim to reduce congestion on main blockchain networks while maintaining security guarantees. These solutions include rollups, sidechains, and state channels—each presenting unique blockchain security risks that require specialised mitigation strategies. The investment also targets formal verification tools that mathematically prove smart contract correctness before deployment.

Enterprise blockchain solutions command substantial capital as corporations seek private or consortium blockchain networks with enhanced privacy features and regulatory compliance capabilities. These enterprise-grade platforms must balance the transparency and immutability benefits of blockchain with business requirements for confidentiality and controlled access—a challenge that demands innovative security architectures.

Security-Focused Innovations Receiving Investment

Quantum-Resistant Cryptography development represents a proactive response to emerging blockchain security risks. As quantum computing advances threaten current cryptographic standards, blockchain networks must transition to quantum-safe algorithms. Several projects have received funding to develop and implement post-quantum cryptographic protocols that will protect blockchain networks from future quantum-based attacks.

Decentralised Identity Solutions aim to reduce reliance on centralised authentication systems vulnerable to data breaches. These systems leverage blockchain’s immutability to create verifiable credentials without exposing sensitive personal information. Investment in this sector addresses both security and privacy concerns while enabling seamless cross-platform authentication.

Automated Security Auditing Platforms utilising artificial intelligence and machine learning represent a growing segment of blockchain security investment. These tools scan smart contract code for common vulnerabilities, analyse transaction patterns for suspicious activity, and provide real-time threat intelligence. By automating security analysis, these platforms aim to identify vulnerabilities before they can be exploited.

Cross-Chain Security Protocols receive substantial funding as interoperability becomes essential for blockchain adoption. Bridge protocols incorporating multi-signature schemes, time-locks, and fraud-proof mechanisms attempt to secure asset transfers between disparate blockchain networks. These innovations address one of the most critical blockchain vulnerabilities in today’s multi-chain ecosystem.

Emerging Blockchain Security Risks in 2025 and Beyond

The Rising Threat of AI-Powered Attacks

Artificial intelligence has become a double-edged sword in the blockchain security domain. While AI enhances defensive capabilities, malicious actors increasingly deploy machine learning algorithms to identify and exploit blockchain vulnerabilities at unprecedented speed. AI-powered bots can analyse smart contract code millions of times faster than human auditors, discovering zero-day exploits before security researchers.

Deep learning models enable sophisticated phishing campaigns that create convincing fake wallet interfaces and fraudulent DeFi platforms. These AI-generated scams become increasingly difficult to distinguish from legitimate services, particularly as natural language processing improves. The combination of social engineering tactics with automated vulnerability scanning creates a threat landscape that traditional security measures struggle to counter.

Regulatory Compliance as a Security Vector

As governments worldwide implement blockchain regulations, compliance requirements introduce new blockchain security risks. Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures create centralised data repositories that become attractive targets for hackers. The tension between blockchain’s decentralised ethos and regulatory demands for transparency and control creates architectural vulnerabilities.

Privacy-focused blockchains face particular regulatory challenges. Networks implementing advanced cryptographic techniques like zero-knowledge proofs must balance user privacy with legal requirements for transaction transparency. Regulatory uncertainty itself becomes a security risk, as unclear guidelines may prevent timely security updates or force compromises that weaken overall network security.

Supply Chain Attacks on Blockchain Infrastructure

The blockchain ecosystem relies on extensive infrastructure, including node operators, wallet providers, development libraries, and API services. Supply chain attacks targeting these dependencies have emerged as serious blockchain security risks. Compromised development tools can inject malicious code into smart contracts. Vulnerable third-party libraries become attack vectors affecting multiple blockchain applications simultaneously.

Cloud infrastructure providers hosting blockchain nodes present centralisation risks that contradict the blockchain’s decentralised architecture. Distributed denial-of-service (DDoS) attacks targeting major cloud platforms can temporarily disable significant portions of blockchain networks. This infrastructure dependence creates systemic vulnerabilities that sophisticated attackers can exploit.

Case Studies: When Blockchain Security Risks Became Reality

The Ronin Network Breach: $625 Million Lost

The Ronin Network hack in March 2022 stands as one of the largest cryptocurrency thefts in history, demonstrating how blockchain security risks in validator systems can have catastrophic consequences. Attackers compromised five of nine validator nodes controlling the network’s bridge, enabling them to forge withdrawals of 173,600 ETH and 25.5 million USDC tokens.

This incident highlighted critical blockchain vulnerabilities in multi-signature schemes with insufficient decentralisation. The Ronin sidechain, designed to support the popular game Axie Infinity, prioritised transaction speed and low fees over security redundancy. The concentration of validator control among related entities created a single point of failure that sophisticated attackers exploited through targeted social engineering and system infiltration.

Poly Network Exploit: A White Hat Twist

The Poly Network hack in August 2021 initially appeared as a $611 million disaster, but it evolved into an unusual story when the hacker returned the stolen funds. This cross-chain protocol exploit revealed fundamental blockchain security risks in bridge architecture. The attacker manipulated the contract’s keeper function, allowing unauthorised control over cross-chain transactions.

Despite the positive resolution, this incident exposed how cross-chain communication protocols represent some of the most significant blockchain vulnerabilities in decentralised finance. The attack demonstrated that even well-audited code can contain logic flaws that enable complete protocol takeover. The complexity of cross-chain messaging creates attack surfaces that traditional single-chain security audits may overlook.

Terra/LUNA Collapse: Algorithmic Vulnerabilities

The May 2022 collapse of the Terra ecosystem, wiping out approximately $40 billion in value, illustrated blockchain security risks extending beyond traditional hacking. The algorithmic stablecoin UST relied on economic incentives and the LUNA token to maintain its dollar peg. When market conditions created a death spiral, the mechanism failed catastrophically.

This case demonstrated that blockchain vulnerabilities encompass protocol design flaws and economic attack vectors, not just technical exploits. The incident sparked intense debate about algorithmic stablecoin security and whether mathematical models can adequately account for extreme market conditions and potential malicious coordination. It highlighted the importance of stress-testing blockchain protocols against adversarial scenarios that push system parameters beyond normal operating conditions.

Technological Solutions Addressing Blockchain Security Risks

Formal Verification and Mathematical Proofs

Formal verification represents a paradigm shift in addressing blockchain security risks through mathematical rigour rather than empirical testing. This approach uses logical proofs to verify that smart contract code behaves exactly as intended under all possible conditions. Unlike traditional auditing that tests specific scenarios, formal verification provides mathematical guarantees about program correctness.

Several blockchain projects now require formal verification for critical smart contracts, particularly those managing substantial value. Tools like Coq, Isabelle, and K Framework enable developers to specify intended contract behaviour formally and prove implementation correctness. While formal verification significantly increases development time and cost, it eliminates entire classes of blockchain vulnerabilities that arise from coding errors and unexpected edge cases.

Zero-Knowledge Proofs: Enhancing Privacy and Security

Zero-knowledge cryptographic protocols address blockchain security risks related to privacy while maintaining transaction validity. These mathematical techniques allow one party to prove knowledge of information without revealing the information itself. ZK-SNARKs (Zero-Knowledge Succinct Non-Interactive Arguments of Knowledge) and ZK-STARKs (Zero-Knowledge Scalable Transparent Arguments of Knowledge) enable private transactions on public blockchains.

Beyond privacy, zero-knowledge proofs enhance scalability through rollup technologies that bundle thousands of transactions into a single proof verified on-chain. This approach reduces blockchain congestion while maintaining security guarantees. As quantum computing threatens traditional cryptographic schemes, zero-knowledge proofs offer potential quantum-resistant alternatives that could secure blockchain networks against future computational advances.

Multi-Party Computation for Distributed Key Management

Multi-party computation (MPC) addresses blockchain security risks associated with private key management by distributing key generation and signing across multiple parties. No single participant possesses the complete private key, eliminating single points of failure. MPC protocols enable threshold signatures where a predetermined number of parties must cooperate to authorise transactions.

This technology proves particularly valuable for institutional cryptocurrency custody, where security requirements exceed individual wallet capabilities. MPC-based wallets eliminate the risk of insider threats while maintaining operational efficiency. Advanced MPC protocols now support dynamic party sets, allowing participant rotation without regenerating keys—a crucial feature for long-term security in enterprise blockchain applications.

Hardware Security Modules and Secure Enclaves

Specialised hardware provides additional defence layers against blockchain vulnerabilities by creating isolated execution environments for sensitive cryptographic operations. Hardware Security Modules (HSMs) store private keys in tamper-resistant devices, making key extraction extraordinarily difficult even if surrounding systems are compromised. Trusted Execution Environments (TEEs) like Intel SGX create secure enclaves within general-purpose processors.

These hardware-based solutions address both external attacks and insider threats by ensuring that critical operations occur in environments protected from both network-based exploits and privileged system administrators. While hardware security adds complexity and cost, it provides defence-in-depth for high-value blockchain applications where software-only solutions prove insufficient.

The Human Factor in Blockchain Security Risks

Social Engineering and Phishing Attacks

Despite technological sophistication, human vulnerability remains among the most exploitable blockchain security risks. Phishing campaigns targeting cryptocurrency users have grown increasingly sophisticated, using fake wallet interfaces, fraudulent customer support channels, and impersonation of trusted community figures. These attacks bypass technical security measures by manipulating users into revealing private keys or approving malicious transactions.

The irreversible nature of blockchain transactions amplifies the impact of social engineering. Unlike traditional financial systems offering fraud protection and transaction reversal, blockchain users who fall victim to phishing attacks have virtually no recourse. Education and user experience design become critical security components, yet many blockchain applications prioritise functionality over intuitive security interfaces.

Insider Threats in Blockchain Organisations

Centralised elements within nominally decentralised systems create blockchain vulnerabilities exploitable by insiders. Exchange employees with privileged access, core development team members with repository control, and validator operators with network influence all represent potential insider threats. Several major cryptocurrency thefts have involved inside assistance or complete insider execution.

Organisational security practices, including background checks, access controls, and monitoring systems, address these risks but introduce centralisation that conflicts with blockchain philosophy. The tension between operational security and decentralisation creates architectural trade-offs that every blockchain project must navigate based on its specific threat model and trust assumptions.

Developer Errors and Code Quality Issues

The blockchain development community faces a significant talent shortage, with demand for experienced smart contract developers far exceeding supply. This skills gap contributes to blockchain security risks as inexperienced developers create vulnerable code deployed on immutable networks. Once deployed, buggy smart contracts cannot be easily patched, and any vulnerabilities become permanent attack vectors.

Code reuse and dependency on external libraries increase development efficiency but introduce supply chain risks. Vulnerabilities in widely used libraries affect multiple projects simultaneously. The rapid pace of blockchain innovation often prioritises speed-to-market over comprehensive security testing, creating an ecosystem where flawed code manages billions in assets.

Regulatory Landscape and Its Impact on Blockchain Security Risks

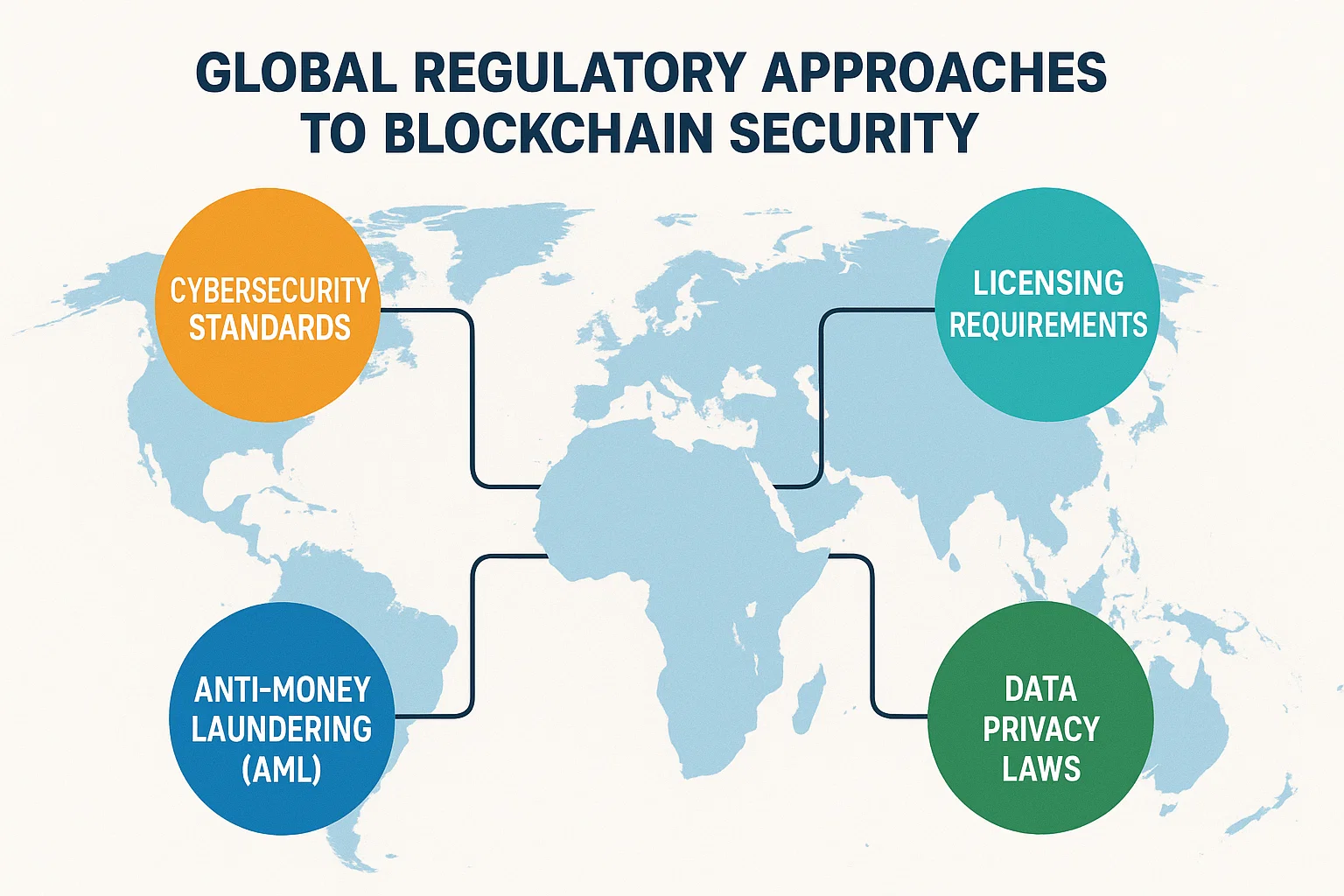

Global Regulatory Approaches to Blockchain Security

Governments worldwide have adopted varied approaches to blockchain regulation, each with implications for blockchain security risks. The European Union’s Markets in Crypto-Assets (MiCA) regulation establishes comprehensive frameworks for cryptocurrency service providers, including security and operational resilience requirements. These regulations mandate specific security controls, regular audits, and incident reporting procedures.

In contrast, the United States has pursued fragmented regulation across multiple agencies, creating uncertainty that some argue increases blockchain vulnerabilities by discouraging security investment and best practice standardisation. Asia-Pacific nations range from Singapore’s innovation-friendly regulatory sandbox approach to China’s restrictive policies prohibiting many blockchain activities. This regulatory patchwork creates compliance challenges for global blockchain projects while leaving security gaps in jurisdictions with minimal oversight.

Compliance Requirements Driving Security Innovation

Regulatory compliance demands have paradoxically driven security innovation while introducing new risks. Data protection regulations like GDPR create tension with blockchain’s immutability—how can “right to be forgotten” coexist with permanent ledgers? Solutions include off-chain data storage with on-chain hashes, encryption with deletable keys, and private blockchains with selective disclosure capabilities.

Financial regulations requiring customer due diligence force blockchain projects to implement identity verification systems, creating centralised databases that become attack targets. The challenge lies in satisfying regulatory requirements without undermining the security and privacy properties that make blockchain valuable. Some projects implement privacy-preserving compliance through zero-knowledge proofs, enabling regulatory oversight without exposing sensitive user data.

Security Standards and Certification Programs

Industry initiatives establishing security standards help address blockchain security risks through best practice codification and third-party validation. Organisations like the Blockchain Security Alliance, CryptoCurrency Certification Consortium, and various national standards bodies have published security frameworks for blockchain applications. These standards cover development practices, operational security, incident response, and audit procedures.

Certification programs provide users with security assurance signals, though certification quality varies significantly across providers. Some certifications require rigorous technical audits and ongoing monitoring, while others involve minimal verification. As blockchain adoption grows, distinguishing credible certification programs from security theatre becomes increasingly important for risk management.

Future Outlook: Can Innovation Outpace Blockchain Security Risks?

The Quantum Computing Threat Timeline

Quantum computers capable of breaking current blockchain cryptography remain years away, yet this looming threat shapes current security investment priorities. Most blockchain networks use elliptic curve cryptography vulnerable to quantum algorithms like Shor’s algorithm. Post-quantum cryptographic algorithms resistant to quantum attacks require larger key sizes and more computational resources, creating performance trade-offs.

Blockchain networks must implement quantum-resistant cryptography before large-scale quantum computers emerge—a transition requiring years of testing and gradual migration. Some projects have begun researching quantum-safe signature schemes, but ecosystem-wide adoption faces coordination challenges. The timeline uncertainty around quantum computing development creates difficult decisions about when to prioritise quantum resistance versus more immediate blockchain security risks.

Artificial Intelligence in Threat Detection and Response

Machine learning systems increasingly monitor blockchain networks for anomalous patterns indicating attacks or exploits. These AI-powered security tools analyse transaction flows, smart contract interactions, and network behaviour to identify threats in real-time. Pattern recognition algorithms can detect suspicious activity that human analysts might miss, particularly in high-frequency trading environments where attacks occur in seconds.

However, adversarial machine learning techniques enable attackers to evade AI-based detection systems. The arms race between AI security tools and AI-powered attacks will shape future blockchain vulnerabilities. Defensive AI requires continuous training on evolving attack patterns, creating ongoing costs for blockchain security operations. The integration of AI security tools with automated response mechanisms promises faster threat mitigation but introduces new risks around false positives and system manipulation. Centralised

Security Solutions and Bug Bounty Programs

Community-driven security initiatives represent a distinctive approach to managing blockchain security risks by leveraging open-source principles. Public bug bounty programs reward security researchers for responsibly disclosing vulnerabilities before malicious exploitation. Leading blockchain projects now offer substantial rewards—sometimes exceeding $1 million—for critical vulnerability discoveries.

Decentralised security auditing through community review provides continuous monitoring that formal audits cannot match. Open-source code enables thousands of developers to examine implementations, potentially identifying issues that small audit teams might overlook. However, this approach also means attackers have equal access to code for vulnerability research. The transparency trade-off remains central to blockchain security philosophy.

Investment Strategies for Security-Conscious Blockchain Adoption

Due Diligence Framework for Evaluating Blockchain Projects

Investors and enterprises assessing blockchain projects must implement comprehensive security evaluation frameworks. Technical due diligence should examine consensus mechanism design, smart contract audit history, security incident track record, and development team experience. Code quality metrics, test coverage percentages, and formal verification adoption indicate security prioritisation.

Organisational security assessment should evaluate access controls, key management procedures, incident response plans, and security team composition. Projects with experienced security advisors, regular penetration testing, and transparent security policies demonstrate security commitment. Bug bounty program scope and reward levels signal confidence in code quality and willingness to invest in ongoing security.

Risk Mitigation Strategies for Blockchain Users

Individual users can significantly reduce blockchain security risks through proper security hygiene and cautious platform selection. Hardware wallet usage for significant cryptocurrency holdings provides superior security compared to software wallets or exchange custody. Multi-signature arrangements for large transactions add authorisation redundancy that prevents single-point-of-failure losses.

Diversification across multiple blockchain platforms and custody solutions reduces concentration risk. Users should verify transaction details carefully before confirming, particularly for smart contract interactions that may request extensive permissions. Regular security updates, strong unique passwords, and two-factor authentication on all accounts provide basic but essential protection.

Enterprise Blockchain Security Architecture

Organisations implementing blockchain solutions must design security architectures that balance innovation with risk management. Hybrid approaches combining private consortium chains with public blockchain anchoring can provide controlled access while leveraging public network security. Identity and access management systems must enforce least-privilege principles while supporting blockchain’s decentralised operations.

Enterprise blockchain security requires integration with existing cybersecurity infrastructure, including SIEM systems, threat intelligence platforms, and incident response procedures. Regular security assessments, including penetration testing and smart contract audits, should occur throughout development and deployment lifecycles. Disaster recovery and business continuity planning must account for blockchain’s unique characteristics, including transaction irreversibility and distributed state management.

The Verdict: Advancement vs. Risk in the Blockchain Security Race

Current State Assessment

The blockchain industry’s $6.8 billion investment demonstrates s serious commitment to addressing security challenges, yet blockchain security risks continue evolving at alarming rates. Current security solutions address many known vulnerabilities, but new attack vectors emerge as blockchain applications grow more complex. The expanding attack surface from cross-chain bridges, Layer 2 solutions, and DeFi protocols creates opportunities for exploitation that weren’t anticipated in earlier blockchain designs.

Progress in formal verification, zero-knowledge proofs, and hardware security provides genuine advancement in securing blockchain systems. However, security improvements often lag behind feature development and market expansion. The financial incentives for attacking blockchain networks continue growing as cryptocurrency values rise and DeFi locks billions in smart contracts. This creates an adversarial environment where attackers invest substantial resources in discovering and exploiting vulnerabilities.

The Path Forward

Sustainable blockchain security requires shifting from reactive patching to proactive security-by-design approaches. Development practices must prioritise security alongside functionality, with formal verification and comprehensive testing becoming standard rather than exceptional. The industry must invest in developer education, creating a workforce capable of building secure decentralised applications from inception.

Collaboration between blockchain projects, traditional cybersecurity firms, academic researchers, and regulatory bodies will prove essential for addressing systemic blockchain security risks. Information sharing about attacks and vulnerabilities—while potentially embarrassing for affected projects—benefits the entire ecosystem by enabling faster defensive responses. Standards bodies must establish security baselines that balance innovation with user protection.

The fundamental question of whether advancement can outpace blockchain security risks lacks a simple answer. Technology development provides increasingly sophisticated security tools, yet human factors, economic incentives, and design complexity ensure vulnerabilities will persist. The realistic goal isn’t eliminating all risks but creating resilient systems that detect and recover from security incidents while continuously improving defences against evolving threats.

Conclusion

The $6.8 billion investment in blockchain advancement represents an unprecedented opportunity to build secure, scalable, decentralised systems that could transform how we conduct commerce, manage identity, and coordinate economic activity. Yet this investment must be directed wisely toward solutions that address the root causes of blockchain security risks rather than superficial symptoms. Technical innovations, including quantum-resistant cryptography, formal verification, and advanced key management, provide essential foundations, but technology alone cannot secure blockchain networks.

Success requires holistic approaches combining technical excellence with user education, regulatory clarity, and economic incentives aligned with security. The blockchain community must embrace transparency about security incidents, treating failures as learning opportunities rather than shameful secrets. Organisations building blockchain applications must recognise that security isn’t a one-time expense but an ongoing investment requiring constant vigilance as threats evolve.

Read more: Blockchain Smart Contract Development Services Expert 2025

")